6190 Powers Ferry Road, Suite 505 Atlanta, GA 30339

09.00 to 05.00 ESTMonday to Friday

Succession route: keeping the farm in the family

These strategies are for farmers who have identified a family member to whom they wish to transfer the farming operation.

Determining when to transfer ownership of the operation can be answered different ways:

- Gift and/or sell the farm today

- Gift and/or sell the farm at retirement

- Bequeath and/or sell the farm upon death

Key considerations for the succession route

We recommend that you work closely with an estate-planning attorney to complete the basic planning for your client. Legal documents that may need to be completed include a will or revocable trust, power of attorney and a health care directive.

Lifetime transfer (today or at retirement)

A lifetime transfer is a transaction to arrange a sale, gift of combination of both to a family member.

| Transaction | Arrange sale, gift of combination of both to a family member |

|---|---|

| Legal transactions or documents |

|

| Tax ramifications |

Income-tax ramifications

Gift-tax ramifications

|

| Retirement income |

Proceeds of sale or income stream from installment note can be used for retirement income, which may include annuities and life insurance for supplemental retirement income |

| Concerns |

Loss of control of the farm |

Bargain sale

A bargain sale is a strategy where the farmer sells the operation for a price lower than its fair market value.

For example, the senior farmer sells the operation to the junior farmer for $1 million, when its fair market value is $2 million. The Internal Revenue Service (IRS) will view this transaction as a sale of $1 million and a gift of $1 million. Many times, the sale price is paid as an installment sale using annual cash rents.

BOLD sales support

Contact the Fortress Brokerage Solutions Advanced Sales Team today.

(678)322-3040

(678)322-3040 Info@fortressbrokerage.com

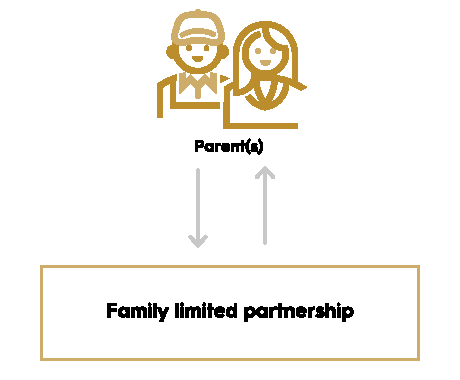

Info@fortressbrokerage.comFamily limited partnership (FLP)

A Family limited partnership (FLP) is a strategy used to move wealth from one generation to another. Partners are either general partners (GP) or limited partners (LP).

One or more general partners are responsible for managing the FLP and its assets. Limited partners have an economic interest in the FLP but typically lack two rights: control and marketability.

- Limited partners have no ability to control, direct or otherwise influence the operations of the FLP. They can neither buy additional assets, nor sell existing assets, and they cannot act on the partnership’s behalf.

- Limited partners also substantially lack the ability to sell their interest, with one typical exception: transfers to immediate family members (spouse, siblings and direct lineal descendants and ascendants). Typically, FLPs are partnerships limited to family members.

- A discount can be placed on the value of the shares, resulting in a smaller gift.

For example, parent(s) set up an FLP and transfer farming operation assets into the partnership.

- Parents transfer farming operation to the FLP

- Parents receive general partner interests in return

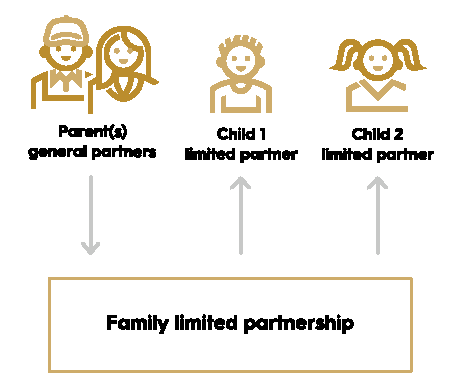

Then, parent(s) gift limited partnership interests to the children.

Parent(s) gift limited partnership interests to the children

Death transfers

Death transfers can include transactions of sales or bequests.

| Transaction |

|

|---|---|

| Legal transactions or documents |

|

| Tax ramifications |

Sale

Bequest

|

- Parents transfer farming operation to the FLP

- Parents receive general partner interests in return

Then, parent(s) gift limited partnership interests to the children.

Parent(s) gift limited partnership interests to the children

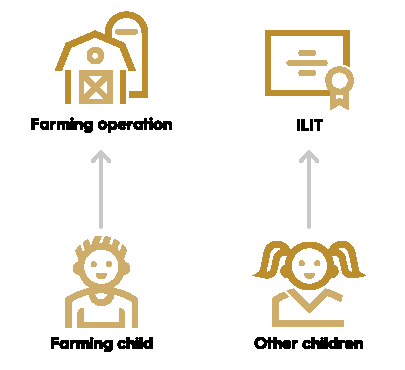

Estate equalization

Estate equalization occurs when the business owner or farmer wants to treat his or her children fairly but maybe not equally.

Here, the owner bequeaths the land or business to a child who wishes to farm the land or continue the business. The rest of the assets then will be split among the other children. Since a large amount of the estate will go to the one child, the owner can equalize the estate by purchasing a life insurance policy and naming the remaining children as beneficiaries of the policy.

The family management strategy

The family management strategy is where the farmer bequeaths the operation into a FLP at the time of death. The farmer can bequeath the entire operation to all children and name one child as a general partner of the operation. Each child will receive income from the operation, and the entire operation will pass from one generation to the next.

The advantages and concerns are the same as an FLP in lifetime transfer.

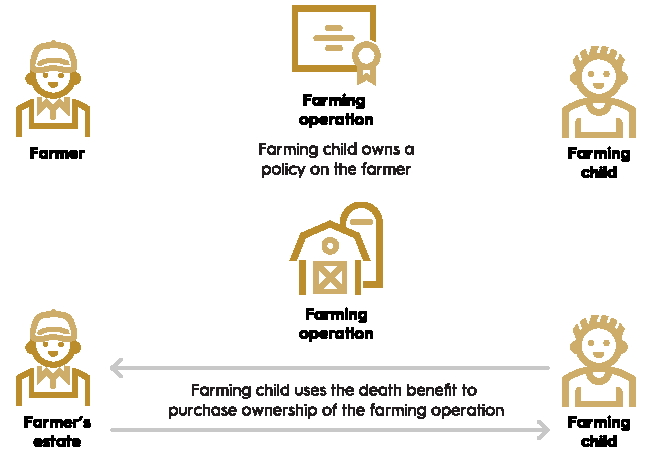

Family buy-sell arrangement

A family buy-sell arrangement consists of the farming child(ren) entering into a buy-sell agreement with the parents, which specifies that they will purchase the land or business upon the death of both parents. This buy-sell arrangement would be funded by the farming child(ren)’s purchase of a life insurance policy on their parents.

Take BOLD action

Key Resources

Additional resources for farm business succession

Learn how to use BOLD with clients

Your business owner clients need life-stage specific tools. We’ll help you find the right solution.

View the step-by-step processLife insurance products contain fees, such as mortality and expense charges, (which may increase over time) and may contain restrictions, such as surrender periods.

Please keep in mind that the primary reason for purchasing life insurance is the death benefit.

Additional agreements may be available. Agreements may be subject to additional costs and restrictions. Agreements may not be available in all states or may exist under a different name in various states and may not be available in combination with other agreements.

Policy loans and withdrawals may create an adverse tax result in the event of lapse or policy surrender and will reduce both the surrender value and death benefit. Withdrawals may be subject to taxation within the first fifteen years of the contract. Clients should consult their tax advisor when considering taking a policy loan or withdrawal.

The Policy Design chosen may impact the tax status of the policy. If too much premium is paid, the policy could become a modified endowment contract (MEC). Distributions from a MEC may be taxable and if the taxpayer is under the age of 59 ½ may also be subject to an additional 10% penalty tax.

An annuity is intended to be a long-term, tax-deferred retirement vehicle. Earnings are taxable as ordinary income when distributed, and if withdrawn before age 59½, may be subject to a 10% federal tax penalty. If the annuity will fund an IRA or other tax qualified plan, the tax deferral feature offers no additional value. Qualified distributions from a Roth IRA are generally excluded from gross income, but taxes and penalties may apply to non-qualified distributions. Please consult a tax advisor for specific information. There are charges and expenses associated with annuities, such as surrender charges (deferred sales charges) for early withdrawals.

This information may contain a general discussion of the relevant federal tax laws. It is not intended for, nor can it be used by any taxpayer for the purpose of avoiding federal tax penalties. This information is provided to support the promotion or marketing of ideas that may benefit a taxpayer. Taxpayers should seek the advice of their own tax and legal advisors regarding any tax and legal issues applicable to their specific circumstances.

For financial professional use only. Not for use with the public. This material may not be reproduced in any way where it would be accessible to the general public.