6190 Powers Ferry Road, Suite 505 Atlanta, GA 30339

09.00 to 05.00 ESTMonday to Friday

Wait-and-See preserves a legacy

Although irrevocable life insurance trusts (ILITs) help solve many estate planning issues, they cannot be changed once established. Taking a wait-and-see approach helps married clients with sizable estates to pass them on despite changing tax laws. A flexible plan allows a client to make needed adjustments throughout a lifetime.

BOLD sales support

Contact the Fortress Brokerage Solutions Advanced Sales Team today.

(678)322-3040

(678)322-3040 Info@fortressbrokerage.com

Info@fortressbrokerage.comWhat is Wait-and-See estate planning

The Wait-and-See One and Two Policy strategies provide a flexible approach — one that uses life insurance and trusts that can be adjusted throughout life’s changing circumstances. So clients can wait and see what life brings.

Benefits of Wait-and-See one policy

Prior to the first death:

- Access to the life insurance policy’s cash value for supplemental retirement income or emergencies.

- Flexibility to make changes throughout your client’s lifetime. Because they own the policy, they can increase or decrease the death benefit and premiums.

- Control over the funding of the policy. They can fund their policy today without giving up control of their assets — which can happen with other estate planning approaches.

- The opportunity to minimize the impact of federal estate taxes.

Considerations of Wait-and-See one policy

- Can only be used with married couples.

- Specific drafting in your client’s estate planning documents needs to be completed to implement the strategy.

- Possible inclusion of death benefit proceeds in their estate.

- Fees and expenses associated with the purchase of life insurance. Policy must be maintained in order to ensure success of strategy.

- If your client lives in a community property state, they and their spouse should sever respective community property interests in the life insurance policy owned by the other spouse. Consult legal counsel on this issue.

Benefits of Wait-and-See two-policy

Prior to the first death:

- Access to the life insurance policy’s cash value for supplemental retirement income or emergencies.

- Flexibility to make changes throughout your client's lifetime. Because they own the policy, they can increase or decrease the death benefit and premiums.

- Control over the funding of the policy. They can fund your policy today without giving up control of the assets – which can happen with other estate planning approaches.

- The opportunity to minimize the impact of federal estate taxes.

Considerations of Wait-and-See two policy

- Can only be used with married couples.

- Specific drafting in estate planning documents needs to be completed to implement the strategy.

- Possible inclusion of death benefit proceeds in the estate.

- Fees and expenses associated with the purchase of life insurance. Policy must be maintained in order to ensure success of strategy.

- If your client lives in a community property state, they and their spouse should sever respective community property interests in the life insurance policy owned by the other spouse. Please consult your local legal counsel on this issue.

Target client

Married business owners who want to own life insurance within their estate, but desire flexibility for estate taxes in the future.

One-policy strategy can be used by:

- Married couples who want life insurance to fund supplemental retirement income and a death benefit to pay estate taxes should they need it.

- Younger people who need the ability to adapt their estate plans to changing circumstances and taxes.

- High net worth couples who already make annual exclusion gifts.

Two-policy strategy can be used by:

- Married couples who want a life insurance death benefit to pay estate taxes should they need it.

- Younger people who need the ability to adapt their estate plans to changing circumstances and taxes.

- Couples who require a first-to-die death benefit for income replacement or other legacy needs.

- Couples in community property states.

Additional estate planning strategies

BOLD highlights several different estate planning strategies to fit your clients needs.

View all strategiesHow does Wait-and-See work?

A wait-and-see estate planning strategy uses a combination of life insurance and trusts that offers clients flexibility to support changing circumstances throughout their lives. It is a strategy for married couples who want to maintain control of and access to life insurance policies that will eventually fund their legacy, estate taxes or both.

There are two wait-and-see approaches.

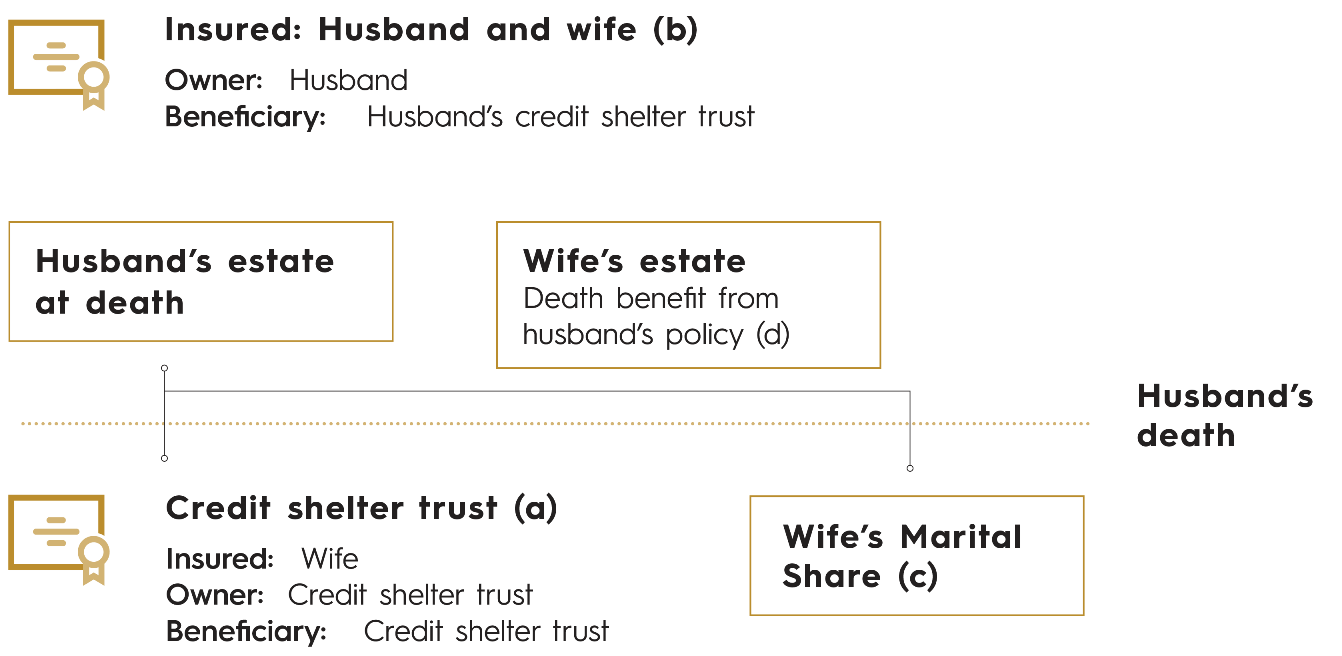

One-policy approach

- A couple applies for a second-to-die life insurance policy(b).

- While the policy covers two lives, once it’s issued, it’s owned by only one of the insureds.

- The insured owning the policy is considered mortality-inferior, or most likely to die first due to age or health considerations. In this example, the husband is the mortality-inferior insured.

- When the husband dies, a credit shelter trust(a) is established. The second-to-die policy is transferred to the credit shelter trust. The owner is changed from the husband to the trust.

- Credit shelter trusts are typically funded with assets that equal up to the Federal Estate Tax Exclusion. When the assets are placed in the trust, they are valued at the fair market value at the time of the husband’s death. The surviving spouse may have limited access to and control of the assets once they are funded in the trust.

- The fair market value of an asset is determined at the time of the owner’s death.

- The fair market value of a life insurance policy is not the death benefit, but an amount close to the policy’s cash value because one insured is still alive.

- Credit shelter trusts are typically funded with assets that appreciate in value. This is because all proceeds in the credit shelter trust, including any appreciation, pass estate and gift tax-free to the beneficiaries upon the wife’s death.

- The remaining assets in the wife’s estate(d) and the Marital Share(c) can be used as a source of income for ongoing expenses.

- Upon the wife’s death, the second-to-die policy(b) pays the death benefit, further funding the credit shelter trust(a).

- Estate taxes are assessed on the wife’s estate(d) and Marital Share(c).

- The proceeds from the credit shelter trust pay any remaining estate taxes due on the wife’s estate(d) and the Marital Share(c).

- The remaining value passes income tax-free to her beneficiaries.

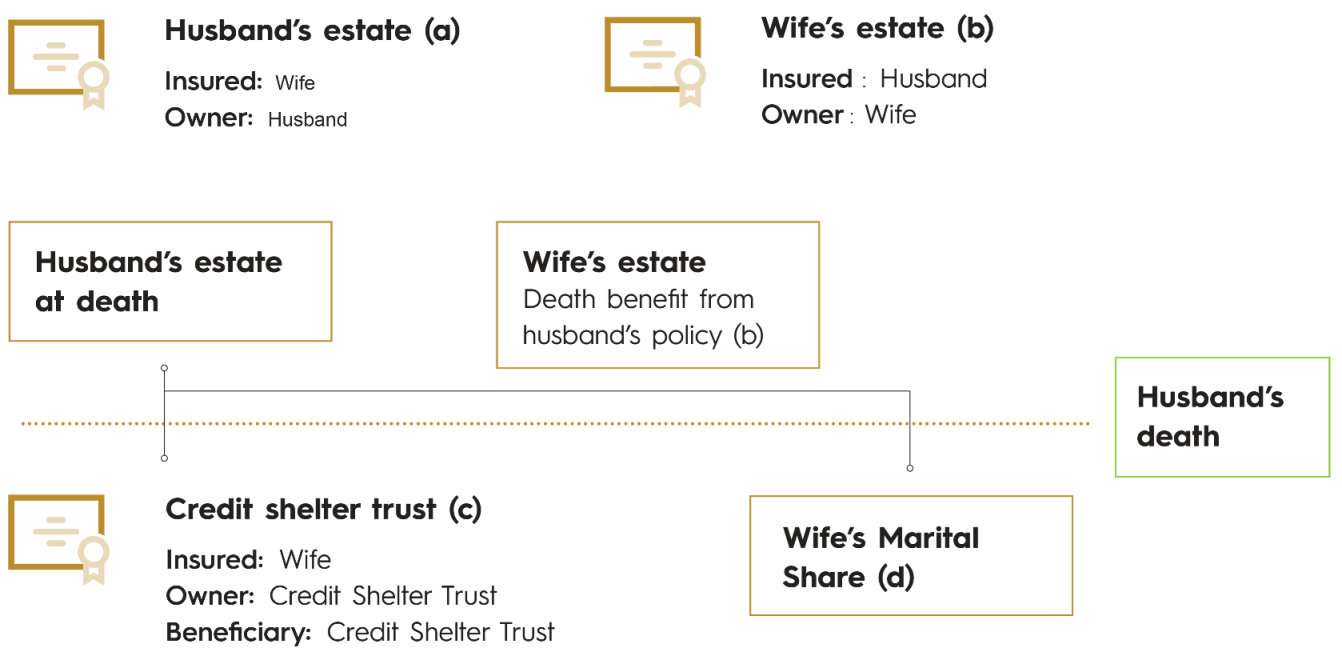

Two-policy approach

- A couple applies for two individual life insurance policies. Each policy is owned by the other spouse.

- When the husband dies, the policy insuring the wife(a) is placed in a Credit Shelter Trust(c) under the husband’s estate. The death benefit from his life insurance policy(b) is paid to his wife. She can use these funds for income replacement or other legacy needs.

- The fair market value of an asset is determined at the time of the owner’s death.

- The fair market value of a life insurance policy is not the death benefit, but an amount close to the policy’s cash value.

- Credit Shelter Trusts are typically funded with assets that appreciate in value. This is because all proceeds in the Credit Shelter Trust, including any appreciation, pass estate and gift tax-free to the beneficiaries upon the wife’s death.

- The remaining assets in the wife’s estate and the Marital Share(d) can be used as a source of income for ongoing expenses.

- Upon the wife’s death, her life insurance pays(a) a death benefit, further funding the Credit Shelter Trust(c).

- Estate taxes are assessed on the wife’s estate and the Marital Share(d).

- The proceeds from the Credit Shelter Trust help pay any estate tax due on the wife’s estate and the Marital Share(d).

- The remaining value passes tax-free to her beneficiaries.

One-policy approach

What if the mortality-superior spouse dies first?

If that happens, the living spouse transfers the second-to-die life insurance policy to an ILIT (irrevocable life insurance trust). But if the surviving spouse dies within the first three years of transferring the policy, the policy is pulled back to their estate. If the couple were to use a survivorship policy with an estate preservation rider that allowed them to buy a four-year term at the mortality-superior spouse’s death, this would not be an issue.

Take BOLD action

Present Wait-and-See to clients

We’ve assembled the tools you need to present to a client in one convenient stop.

Additional resources for Wait-and-See and estate planning

Learn how to use BOLD with clients

Your business owner clients need life-stage specific tools. We’ll help you find the right solution.

View the step-by-step processLife insurance products contain fees, such as mortality and expense charges, (which may increase over time) and may contain restrictions, such as surrender periods.

Please keep in mind that the primary reason for purchasing life insurance is the death benefit.

Additional agreements may be available. Agreements may be subject to additional costs and restrictions. Agreements may not be available in all states or may exist under a different name in various states and may not be available in combination with other agreements.

Policy loans and withdrawals may create an adverse tax result in the event of lapse or policy surrender and will reduce both the surrender value and death benefit. Withdrawals may be subject to taxation within the first fifteen years of the contract. Clients should consult their tax advisor when considering taking a policy loan or withdrawal.

The Policy Design chosen may impact the tax status of the policy. If too much premium is paid, the policy could become a modified endowment contract (MEC). Distributions from a MEC may be taxable and if the taxpayer is under the age of 59 ½ may also be subject to an additional 10% penalty tax.

An annuity is intended to be a long-term, tax-deferred retirement vehicle. Earnings are taxable as ordinary income when distributed, and if withdrawn before age 59½, may be subject to a 10% federal tax penalty. If the annuity will fund an IRA or other tax qualified plan, the tax deferral feature offers no additional value. Qualified distributions from a Roth IRA are generally excluded from gross income, but taxes and penalties may apply to non-qualified distributions. Please consult a tax advisor for specific information. There are charges and expenses associated with annuities, such as surrender charges (deferred sales charges) for early withdrawals.

This information may contain a general discussion of the relevant federal tax laws. It is not intended for, nor can it be used by any taxpayer for the purpose of avoiding federal tax penalties. This information is provided to support the promotion or marketing of ideas that may benefit a taxpayer. Taxpayers should seek the advice of their own tax and legal advisors regarding any tax and legal issues applicable to their specific circumstances.

For financial professional use only. Not for use with the public. This material may not be reproduced in any way where it would be accessible to the general public.