6190 Powers Ferry Road, Suite 505 Atlanta, GA 30339

09.00 to 05.00 ESTMonday to Friday

Split-dollar strategies

Split-dollar strategies split the costs and benefits of a life insurance policy between the employer and employee. Split-dollar arrangements can be effective solutions when an employer wants to protect the business from the loss of a key individual and offer incentives or deferred compensation to its key executives when cost is an issue. The employer and key executive split the policy in one or more ways, cash value, premium, or death benefit. There are two main types of split-dollar strategies.

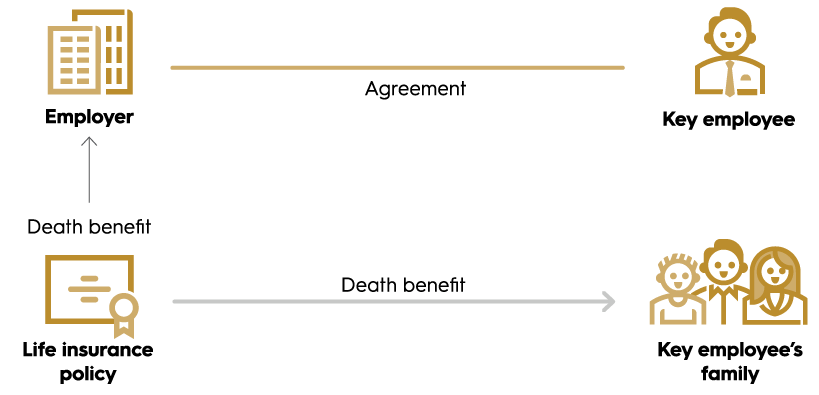

Key person plus is an endorsement split-dollar arrangement using a life insurance benefit paid for and provided by a business for key executives or other key employees. The business owns the policy and pays the premium, and an income tax-free life insurance death benefit is provided to the key employee’s family or other chosen beneficiary.

- Employer-financed life insurance

- Key person plus — Endorsement split-dollar arrangement

Employer-financed life insurance

Employer-financed life insurance is an equity collateral assignment split-dollar strategy that allows a business to provide life insurance for an owner, key executive or other key employee.

Although the employee owns the policy, the business pays the premiums as a loan to the employee. The policy is assigned to the employer as collateral for the loaned premium, and the executive names a beneficiary of the policy’s income tax-free death benefit.

There are two possible tax methods that can be used with employer-financed life insurance:

- If the economic benefit method of taxation is used, the business receives a portion of the death benefit equal to the greater of the cash value of the contract or the business’s premiums paid.

- If the loan method is used, a portion of the death benefit equal to the premiums loaned or cash surrender value is paid to the business.

Key person plus — Endorsement split-dollar arrangement

Key person plus is an endorsement split-dollar arrangement using a life insurance benefit paid for and provided by a business for key executives or other key employees. The business owns the policy and pays the premium, and an income tax-free life insurance death benefit is provided to the key employee’s family or other chosen beneficiary.

Why choose employer-financed life insurance

How employer-financed life insurance works

The policy is collaterally assigned to the business to secure its interest in the policy.

The amount assigned to the business depends on which tax method is used for the arrangement.

- If the loan method is used, a portion of the death benefit equal to the premiums loaned or cash surrender value is paid to the business.

- The company loans money to an executive to pay premium on a permanent life insurance policy, which accumulates cash value.

- The executive purchases a policy. Working with a licensed attorney, a split-dollar agreement is established that collaterally assigns a portion of the death benefit to the company.

- The executive names a beneficiary.

At rollout or at the executive’s death, the company receives a portion of the policy’s cash value equal to the premiums paid, plus interest. The executive or the executive’s family receive the balance of the policy’s death benefit or cash value.

Why choose key person plus

How key person plus works

- Company purchases a permanent life insurance policy on the life of the executive and pays all premiums

- Company owns the policy and endorses a portion of the death benefit to the executive as a pre-retirement survivor benefit

- Executive is taxed on the economic benefit of the premium based on the issuing insurance company’s term rates or a table of rates provided by the Internal Revenue Service (IRS)

If the executive dies while employed by the company:

The company receives a portion of the death benefit to recover its costs; the executive’s beneficiaries receive the balance.

When the executive retires:

The arrangement is terminated:

- Company retains ownership of the policy

- When the executive dies, the company recovers the cost of the arrangement through the death benefit proceeds of the policy

- Company may choose to transfer the policy to the executive as a taxable bonus

Employer financed split-dollar taxation

Key employee income taxes

- Any interest paid to the business by the key employee or the trust for the loaned premiums is not deductible to the key employee.

- If the interest due is not paid to the business, the interest amount is deemed income taxable to the key employee.

- If the split-dollar agreement is terminated, the key employee or trust must pay back premiums paid or any other outstanding loan amount.

- The death benefit paid to the insured’s chosen family member is income tax-free.

Employer income taxes

- The business cannot income tax deduct the premiums paid.

- If the business is a flow-through tax entity such as a partnership, S corporation or LLC, the owners of the business are taxed on their pro-rata share of the nondeductible premium.

- Any interest paid to the business for the loaned premiums is taxable to the business.

Employer-financed life insurance benefits and considerations

Benefits

Employer

- Employee owns the policy

- Flexible and minimal administrative costs

- Company can select employees it wants to reward

Employee

- Affordable death benefit coverage for employee

- Death benefit paid to insured’s beneficiary income tax-free

- Ability to exclude death benefit from estate with proper planning

Considerations

Employer

- No income tax deduction for premium payments

- Special issues for flow-through tax entities (LLCs, partnerships, etc.)

- Costs may not be fully recovered

- Attorney fees for drafting agreement

- Any interest paid to company for loaned premium is taxable to company

Employee

- Taxed annually; method depends on type of taxation option chosen (loan or economic benefit)

- Must be acceptable underwriting risk

- Death proceeds may be included in estate

- Subject to employer’s creditors

Key person plus taxation

Below are the tax results of endorsement split-dollar using the economic benefit method of taxation:

Key employee income taxes

- The key employee is taxed annually on both Minnesota Life Insurance Company and Securian Life Insurance Company’s one-year annually renewable term (ART) policy costs, and the Table 2001* costs. This is the “economic benefit.”

- If the policy is a second-to-die policy, both Minnesota Life Insurance Company and Securian Life Insurance Company’s one-year ART-SD term policy costs or the extrapolated second-to-die Table 2001* costs are taxed annually to the key employee.

- The death benefit paid to the insured’s chosen family member is income tax-free.

Employer income taxes

- Premiums are not tax deductible for the business.

- If the business is a flow-through tax entity such as a partnership, S Corporation or LLC, the business owners are taxed on their pro-rata share of the nondeductible premium.

- The business cannot income tax deduct the one-year term costs or Table 2001* costs that are taxed to the key employee (insured).

- Assuming that the business met the employer owned life insurance (EOLI) rules before the policy was issued, the death benefit paid to the business should be income tax-free.

Key person plus benefits and considerations

Benefits

Employer

- Provides a way to reward select key employees

- Cost recovery

Employee

- Provides income to surviving family/beneficiaries in event of death prior to retirement

Considerations

Employer

- Premiums are not income tax deductible

- Must comply with notice and consent rules for EOLI before policy issuance

- Attorney fees

Employee

- Taxed annually on the economic benefit value of the death benefit provided

- Must be acceptable underwriting risk

- Death proceeds may be included in estate without additional planning

- Subject to employer’s creditors

BOLD sales support

Contact the Fortress Brokerage Solutions Advanced Sales Team today.

(678)322-3040

(678)322-3040 Info@fortressbrokerage.com

Info@fortressbrokerage.comTake BOLD action

Key resources

Get access to these and other tools on our secured website for financial professionals.

Strategy-specific marketing tools

Learn how to use BOLD with clients

Your business owner clients need life-stage specific tools. We’ll help you find the right solution.

View the step-by-step processLife insurance products contain fees, such as mortality and expense charges, (which may increase over time) and may contain restrictions, such as surrender periods.

Please keep in mind that the primary reason for purchasing life insurance is the death benefit.

Additional agreements may be available. Agreements may be subject to additional costs and restrictions. Agreements may not be available in all states or may exist under a different name in various states and may not be available in combination with other agreements.

Policy loans and withdrawals may create an adverse tax result in the event of lapse or policy surrender and will reduce both the surrender value and death benefit. Withdrawals may be subject to taxation within the first fifteen years of the contract. Clients should consult their tax advisor when considering taking a policy loan or withdrawal.

The Policy Design chosen may impact the tax status of the policy. If too much premium is paid, the policy could become a modified endowment contract (MEC). Distributions from a MEC may be taxable and if the taxpayer is under the age of 59 ½ may also be subject to an additional 10% penalty tax.

An annuity is intended to be a long-term, tax-deferred retirement vehicle. Earnings are taxable as ordinary income when distributed, and if withdrawn before age 59½, may be subject to a 10% federal tax penalty. If the annuity will fund an IRA or other tax qualified plan, the tax deferral feature offers no additional value. Qualified distributions from a Roth IRA are generally excluded from gross income, but taxes and penalties may apply to non-qualified distributions. Please consult a tax advisor for specific information. There are charges and expenses associated with annuities, such as surrender charges (deferred sales charges) for early withdrawals.

This information may contain a general discussion of the relevant federal tax laws. It is not intended for, nor can it be used by any taxpayer for the purpose of avoiding federal tax penalties. This information is provided to support the promotion or marketing of ideas that may benefit a taxpayer. Taxpayers should seek the advice of their own tax and legal advisors regarding any tax and legal issues applicable to their specific circumstances.

For financial professional use only. Not for use with the public. This material may not be reproduced in any way where it would be accessible to the general public.